by Martin Davies

In the previous article, I highlighted Papua New Guinea’s (PNG’s) ongoing problem with a shortage of foreign exchange (forex), the causes of this shortage, and that because of forex rationing has led to a large backlog of orders. The existence of the backlog indicates that the currency is out of alignment with its market value over a sustained period of time. In this second article, I talk about the current imbalances in the economy due to the overvaluation of the kina, how big that overvaluation is, and what would happen if the kina depreciated.

As part of the report (being summarised in this three-part series), we present a new approach to determining the equilibrium real exchange rate (ERER) for PNG. First, let’s define the real exchange rate (RER), and the ERER. The RER measures the rate at which PNG’s goods can be converted into foreign goods (the number of PNG goods per unit of foreign goods). This is determined by a number of factors, notably the foreign and domestic price levels, and the nominal exchange rate (the number of kina per US dollar). The RER indicates how competitive PNG goods are in comparison to goods from other countries.

The ERER is the RER that will lead to internal balance and external balance. What are internal and external balances? They are two desirable outcomes or objectives which economic policymakers seek to achieve. Movement away from either or both of these outcomes can be painful for the economy and its populace.

Simply put, internal balance means that the resources in the economy are fully employed, a desirable situation in which most people who want a job can get a job. External balance means that the kina is fully convertible (using kina you can buy as much forex as you want at the prevailing exchange rate) without resorting to unsustainable foreign borrowing.

In terms of these objectives, PNG currently has high unemployment and a non-convertible currency, which is known as a ‘deficit-unemployment’ situation.

In the report, we adjust the standard internal-external balance model for features of the PNG economy, which includes a large resource sector that is mainly foreign-owned. A feature of this new approach is that it enables us to determine the influence of changes in the government takes on the ERER. As noted in the first article, government take is the ratio of fiscal resource revenue to total resource sector output, or more simply put, the fraction of resource sector output that is returned to the government.

The model suggests that the RER should depreciate in response to a fall in the terms of trade, an increase in the fiscal deficit, and a fall in the government take in order to maintain both internal and external balance.

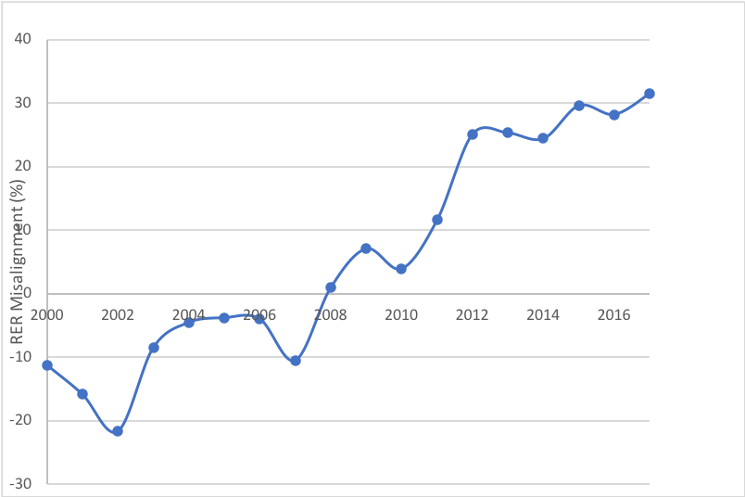

In the report, we estimate PNG’s ERER over the past 20 years (see Figure 1) and find that the current RER is overvalued by between 20% and 30%. This means that the kina needs to depreciate now.

Figure 1: RER misalignment estimates based on government take, 2000-2017

We estimate that a 20% depreciation of the RER will have the following effects.

- It will improve the trade balance by an amount exceeding USD250 million per annum, increasing forex inflows by the same amount.

- It will increase real agricultural export income by over 30%.

- It will stimulate economic activity in the export and import-competing sectors, providing much-needed stimulus to non-resource sector economic activity.

- It will cause a redistribution of income from urban to rural households; however, some of the falls in urban income will be moderated by the increase in non-resource sector activity. This will increase the relative attractiveness of being located in a rural setting relative to an urban one, which could slow urban drift.

- It will stimulate the forex inflows from overseas investors, as it brings the kina exchange rate into closer alignment with market participants’ beliefs about the equilibrium rate.

- Given pass-through from a nominal depreciation to the price level of 40%, it will increase the domestic price level by approximately 13%.

- It will lead to an increase in the kina value of PNG’s foreign debt, both private and government-held. This will be offset by higher growth through the stimulus to the tradable sector, and the relaxation of forex rationing by the Bank of Papua New Guinea. Offsetting effects for firms include an increase in profits due to higher growth and better access to forex, which reduce costs and allow for remittance of profits and dividends.

We recommend a 20% depreciation of the RER. This would require a 33% depreciation of the nominal exchange rate (kina relative to the US dollar) given the pass-through to domestic prices of around 40%, not including any depreciation necessary to offset PNG’s positive inflation differential with its trading partners. This is quite a large adjustment, but there is no alternative.

The final article in this series looks at other reforms to tackle the forex backlog and rationing.

Disclosure: This research was funded by the Australian Government through the Department of Foreign Affairs and Trade at the request of the Government of Papua New Guinea, through the Department of Treasury. The views expressed in the report are those of the author only.

This article appeared first on Devpolicy Blog (devpolicy.org), from the Development Policy Centre at The Australian National University. It is the second blog in a series on #Kina convertibility.

Martin Davies is Associate Professor of Economics at Washington Lee University, Visiting Associate Professor at the School of Business and Public Policy, UPNG, and Visiting Fellow at the Development Policy Centre, ANU.